Defined Benefit Transfer Considerations

Defined Benefit Pension Transfer Values

If you have a Defined Benefit (DB) Pension there is a reasonable chance that you are being offered the option to transfer this into the more common type of pension (Defined Contribution). This is a big decision and an irreversible one, so it’s important to understand exactly what this means, and what the pros and cons for you might be.

Final Salary/Defined Benefit Scheme

A defined benefit or DB Pension (also known as final salary pension) is a special type of workplace pension. Instead of building up a pension pot over time, it provides you with a guaranteed annual income for life, based on your final or average salary (hence the name).

DB pensions are most often provided by the public sector and government employers. Some private sector employers do still offer them however a number of the private sector schemes have ceased accruing benefits for future service. Historically, a DB Pension has been seen as the most attractive pension arrangement for employees.

Key Benefits

DB pensions are often seen as more generous, because it would take an above – average defined contribution (DC) pot to be able to buy an annuity that pays the same amount as a DB scheme. What’s more, the payouts from a DB pension are guaranteed for the rest of your life. So long as the pension scheme remains funded, your pension income will be paid no matter how long you live. There is also typically a spouse’s pension in the event of death.

Drawbacks

Despite the attractions of a DB pension, in some ways it is not as flexible as a DC pension pot. You can’t vary the income you take from it, nor draw out larger lump sums (apart from the tax-free lump sum offered by some final schemes).

The DB pension cannot be inherited by your beneficiaries, If you die prematurely, there will be a widow’s pension for your spouse, but most of the benefits will be lost, and nothing passes to your estate.

Also, there is the small risk that your pension scheme may collapse at some future point, if it is no longer adequately funded (e.g. employer becomes insolvent).

What is a Transfer Value?

You can ‘trade in’ a DB pension for a fixed-size pot of the kind found in defined contribution (DC) pension schemes. That equivalent value (i.e. the ‘transfer value’) is calculated actuarially to estimate the monetary amount that would be required to provide the equivalent guaranteed income, based on market conditions at the date of calculation.

Taking a transfer value involves giving up the certainty of income for life in order to take control of the investment of the fund that underpins the defined benefit pension. The individual would then use the fund under the defined contribution arrangement to provide an income over the course of retirement which may be less or greater than the defined benefit pension given up.

The transfer option offers greater flexibility on how you take your benefits at the expense of certainty.

There are potentially significant risks, in particular, investment risk with taking the transfer value and professional advice should be sought before making this decision. The key risks that do not apply to a DB pension are as follows:

The value is subject to investment performance and there is risk of capital loss

The investment performance is worse than anticipated and the value is exhausted prior to death

Significant withdrawals are taken early or the individual lives longer than expected

Changes in Transfer Values

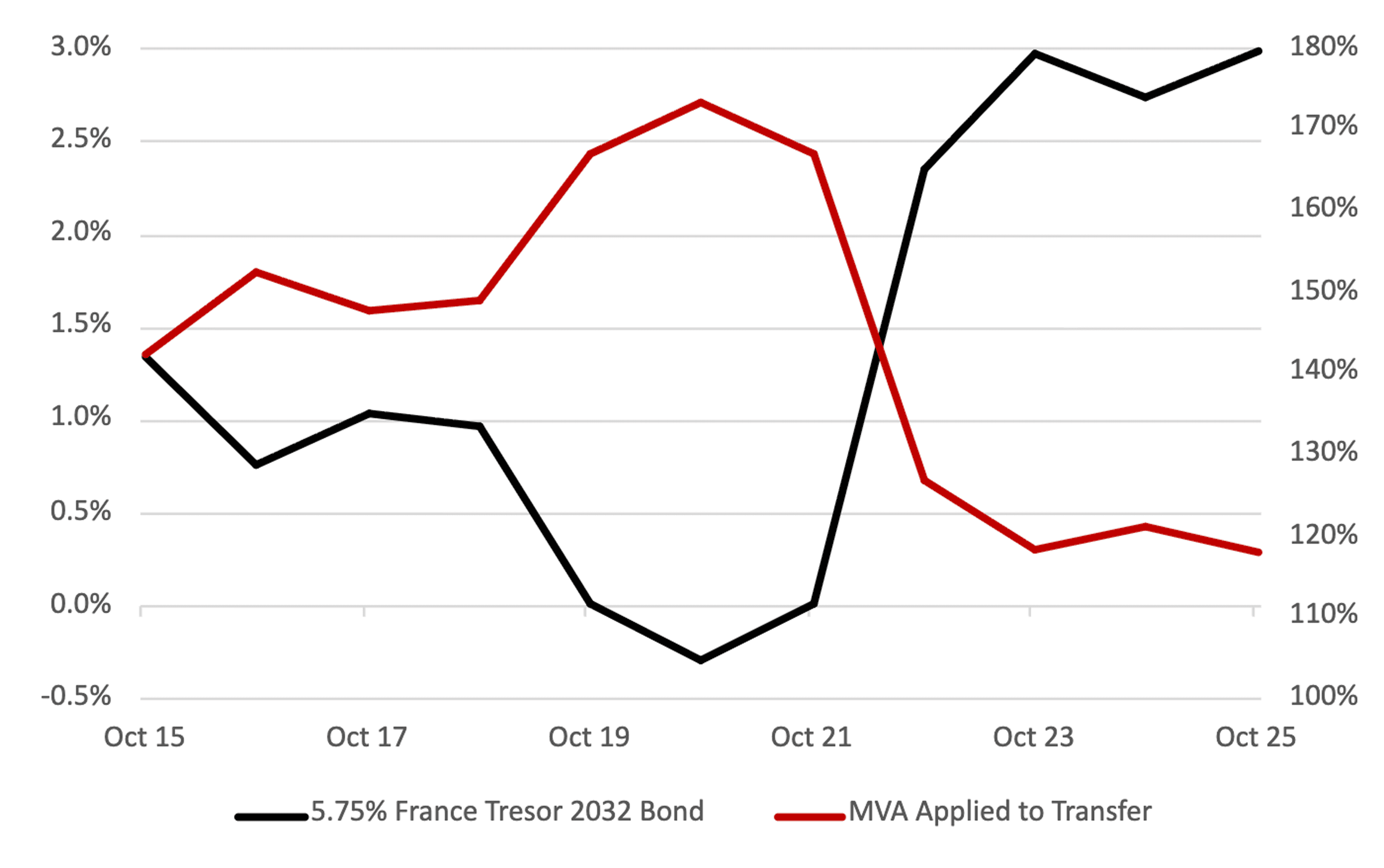

The defined benefit transfer value is calculated in line with statutory guidance issued by the Pensions Authority and the Society of Actuaries in Ireland. As part of this calculation, a Market Value Adjustment (MVA) is applied to reflect prevailing economic conditions at the time of assessment.

The MVA is derived with reference to the yield on the France Trésor 2032 long-term government bond, which acts as a benchmark for discounting future liabilities. The chart below illustrates how this yield has evolved over the past decade and the corresponding impact on the MVA.

Over the period from October 2014 to October 2024, bond yields have increased from 1.83% to 2.74%, resulting in a reduction in the MVA from 135% to 121%. This demonstrates the inverse relationship between interest rates and transfer value adjustments: when yields were at historic lows around 2020, MVAs were significantly higher, making transfer values more attractive. However, with interest rates rising again in recent years, MVAs have adjusted downwards, leading to less favourable transfer values.

Factors to Consider

As you can see from the graph, even minor changes in the bond yield can have a significant effect on the transfer values. For those who are considering the transfer option, the interest rate movements need to be taken into consideration along with the following:

Does the flexibility of the transfer value meet my requirements in retirement?

Do I want to manage my own wealth and am I willing and able to take on the investment risk that this incurs?

Is passing wealth to the next generation a requirement?

How secure is the existing Defined Benefit Scheme?

How does the decision fit in with my other non pension assets and income?

If you have any questions on the above information please don’t hesitate to contact us.

Brendan Nordon 13/11/2025